Financial Planning

How your personal inflation rate could help protect your wealth

As the world continues to deal with the Covid pandemic, and now the Russian invasion of Ukraine, it seems higher inflation could be around for longer than initially feared.

As energy and fuel prices continue to spiral and the cost of other household goods increase, the Guardian reports that experts now predict inflation will reach 8% by April 2022.

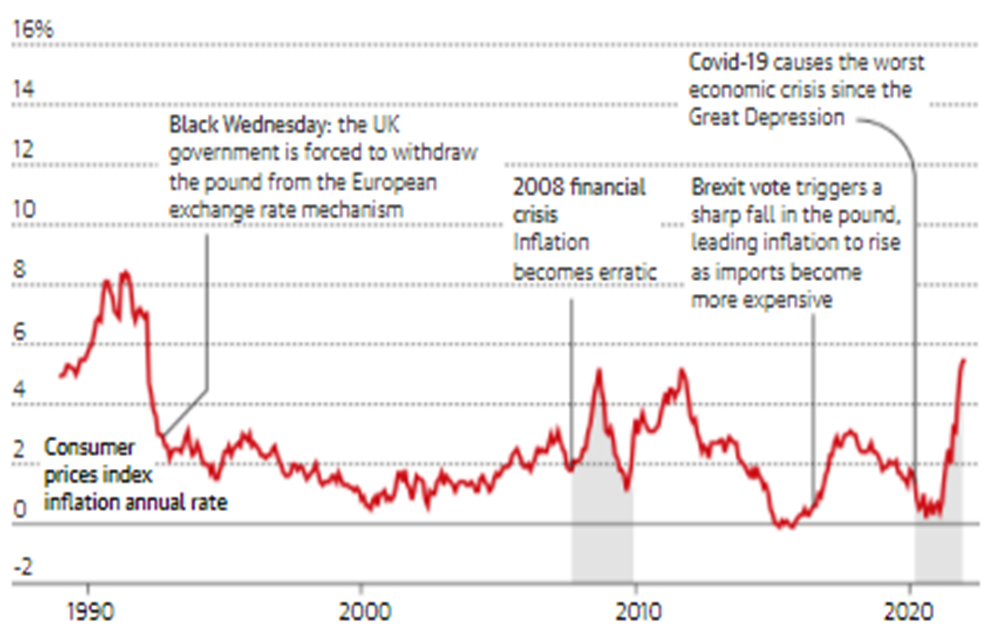

The report came as the Office for National Statistics revealed that inflation stood at 5.5% in January 2022. As the chart below shows, it is now higher than it was during the 2008 financial crisis and the Brexit referendum.

Source: the Guardian

While the headlines around inflation can make for depressing reading, what really counts is your personal inflation rate. Knowing what it is could help you adjust your spending and potentially reduce the effects inflation has on your finances.

Read on to learn how inflation is measured and why understanding your personal inflation rate could help you shield your money from its effects.

Inflation is the rising cost of living

Inflation is the increase in the price of goods and services, so can affect everything from your utility bills through to your weekly shop. While a small amount of inflation is seen as vital to a healthy economy, if it becomes too high it can impede economic growth.

More than this, if the increases in your salary or interest earned on savings are not keeping pace with inflation, both could drop in value in real terms.

To demonstrate this, consider the following. If you use an inflation calculator, you need £184 today to have the same spending power as £100 in March 2002.

In other words, your cash needed to grow 84% in the last two decades to keep pace with inflation, which averaged 3.1% a year during the period – significantly below January’s rate of inflation of 5.5%.

So, let’s now consider how the rate of inflation is calculated.

Inflation is calculated using a basket of goods

To calculate the rate of inflation, the Office for National Statistics tracks a “basket” of more than 700 items, which provides around 180,000 prices. These represent the goods and services the average consumer buys, and changes to reflect Britain’s changing shopping habits.

For example, a recent article by the Guardian reveals that in 2022, suits, doughnuts and coal were removed from the list while sports bras, antibacterial surface wipes and meat-free sausages were added.

Every month, the ONS looks at the prices and compares them to the previous year’s figures. The percentage difference is then used to work out the Consumer Price Index (CPI), the UK’s main measure of inflation.

Your spending habits could increase the effects of inflation on your wealth

In reality, this calculation cannot reflect your personal expenditure. This is because the prices of different products will rise at different rates, meaning the effects of inflation will depend on how you spend your money.

For example, if you spend a lot of time in your house, your personal inflation rate could be above the average as you will need to heat it and use electricity. Likewise, if you do a lot of driving or travelling, the cost of fuel could mean you feel the effects of inflation more than those who do not.

So, it’s important to understand your personal rate of inflation, which we will look at now.

Calculating your personal inflation rate is a shrewd move

One way you can calculate your personal inflation rate is to work out your expenditure and compare it to previous years – in much the same way the ONS does when calculating CPI. You could do this on an annual or monthly basis.

This means if you spend £50,000 one year and £55,000 the next, your personal inflation has increased by 10% over the year. Only include regular outgoings and not one-off expenditure, such as the cost of home repairs or a new car.

Alternatively, we can help you establish what your personal inflation rate is.

Knowing your personal rate could reduce inflation’s impact on your money

Understanding what your personal inflation figure is and how you’re spending your money could allow you to alter your expenditure and reduce the effect of cost of living rises on your finances. This might include reducing the amount of driving you do, or turning the heating down at home.

If it transpires your personal rate is higher than the interest you’re receiving on savings, your cash could reduce in value in real terms. One way you could inflation-proof your money would be to consider investing it.

This is because over the long-term, investments typically provide greater growth potential that could negate the effects of inflation on your wealth.

This is backed up by the 2019 Barclays Equity Gilt Study, which tracked the nominal performance of £100 invested in cash, bonds or equities between 1899 and 2019. It revealed that the stock market outperformed cash in 91% of 10-year periods.

It also showed that the original £100 would have been worth around £2.7 million in 2019 if it was put into stocks and shares, compared to just over £20,000 if it had been invested in cash.

Get in touch

If you would like to discuss your personal inflation rate or how you could better shield your wealth from inflation, please contact us by calling 0800 434 6337.

Please note:

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Have My Cake And Eat It

A change in lifestyle