Financial Planning

Compounding: what is it and when is it your best friend or worst enemy?

When one of the greatest minds ever to have lived is said to have called something the “eighth wonder of the world”, it certainly demands our attention. But what was Albert Einstein referring to?

While you might automatically assume it was the science of light or the black holes that are dotted around our universe, you’d be wrong. In fact, the thing he was referring to is not only much closer to home, it’s something that could touch all of our lives in one form or another.

Einstein was referring to compounding, or “compound growth” as investors sometimes call it. It’s a fundamental concept of the financial world, and the reason growth on investments has the potential to mushroom over time.

Conversely though, the “compounding” effect is why debt can do the same.

Read on to discover all you need to know about compounding, and how it can be your financial best friend or worst enemy.

Compounding is growth on the growth you’ve already enjoyed

If you invest money, you expose it to potential growth, something that could be accelerated with compounding. Here’s how.

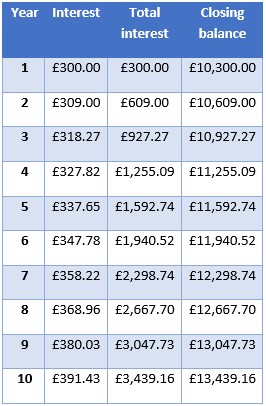

Assume you’re investing £10,000 and you achieve an average 3% growth every year. In year one your money grows by £300 and as long as you leave the growth invested, the following year’s growth is based on £10,300.

As the table below shows, after 10 years your initial investment will be worth nearly £13,500 because of compound interest. Please note the table is for illustration only, and does not take into consideration potential costs of an investment or other factors such as inflation.

Source: the Calculator Site

By comparison, if you had received 3% simple interest, you would have received £300 every year that would have returned £3,000 in total. Compounding has therefore boosted your returns by an additional £439.18.

After 15 years, the extra growth through compounding will be worth £1,079.67, and after 20 years it will be £2,061.11.

Compound growth is why you should invest as early as possible

If you are looking to invest in a Stocks and Shares ISA, pension, or other stock market investment, the earlier you start investing the better as you’re exposing your money to compounding for longer. To demonstrate this, consider the following question.

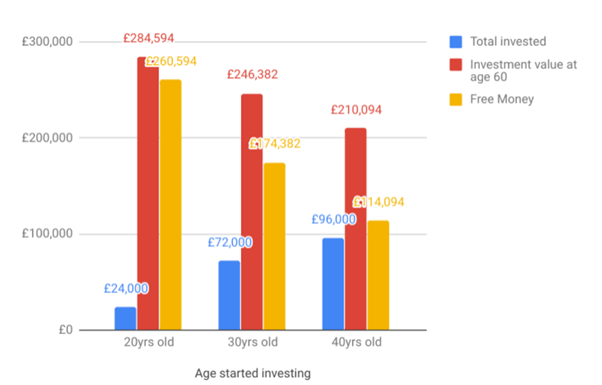

Which of the following scenarios will generate the largest pension pot at the age of 60, assuming a growth rate of 7%?

1. A 20-year-old who invests £200 a month for 10 years, totalling £24,000

2. A 30-year-old who invests £200 a month for 30 years, totalling £72,000

3. A 40-year-old who invests £400 a month for 20 years, totalling £96,000.

As the below graph shows, it’s going to be the 20-year-old, even though he has invested the least.

Source: Money Nest

The reason is that it was invested for the longest period, and therefore enjoyed the most exposure to compounding.

Investing as young as possible into a pension or other long-term investment is critical. As you can see, despite contributing the most, the 40-year-old received the lowest level of growth and smallest return.

Compound interest with debt is dangerous

There is a downside to the idea of compounding, and that’s when it forms part of the interest charged on a debt.

In the same way that growth is boosted by compounding, the interest you pay on debt can be too. This is dangerous if the rate of interest is high, which can be the case with credit cards.

This is because any amount owing will have interest charged on it. If the following month, if you do not pay off the full amount, interest is charged on the outstanding balance, which includes the interest charged the month before.

In the same way you can see additional growth on your investments, your lender is increasing the amount you owe using compound interest.

Little wonder Einstein is quoted as saying this about compounding: “he who understands it earns money, and he who doesn’t, pays it”. This is why it’s important to pay off any amount owing on a credit card every month.

Get in touch

If you would like to discuss how compounding may help boost your wealth, or have a general question about your financial situation or investing, please contact us on 0800 434 6337.

Please note:

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and your financial circumstances.

Have My Cake And Eat It

A change in lifestyle